TMX POV - Shedding Light on the Dark Canadian Market – Deeper Dive into Dark Pools

At Toronto Stock Exchange, we often get asked why traders and investors would want to execute in the Canadian dark markets. Aside from the obvious benefit for investors to hide order flow from predatory behaviour, particularly for larger institutional orders, there are several other reasons and strategies to utilize dark pools when trading in today's complex equities markets.

Let's take a closer look at how dark markets operate in Canada.

How big is the Canadian dark equity market?

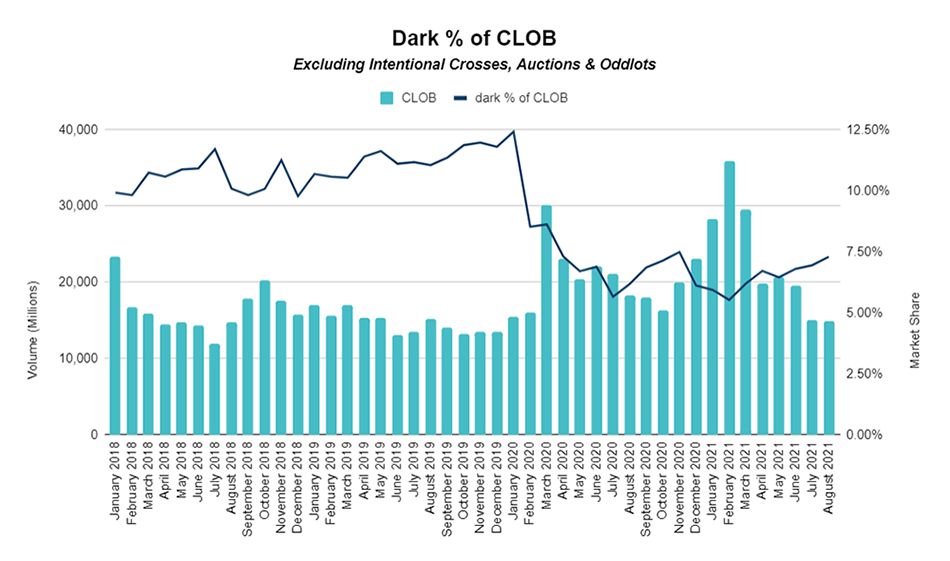

The Canadian equities dark markets are important to our trading community, with a market share that represents approximately 7% of the overall market (excluding international crosses and auctions)*. Dark market share has been stable and increasing slightly over the past couple of years in Canada but decreased somewhat dramatically in Q1 2020 as seen in the chart below, with the introduction of regulatory changes requiring price improvement while trading at-the-touch (i.e. at the national best bid/offer) except for larger executions (greater than 50 boardlots and $30,000 value). We would expect Canadian dark pool market share to increase in the coming years with the introduction of new order types (such as Conditionals), auctions and crosses.

Table 1: Market Intelligence Group of TMX Group

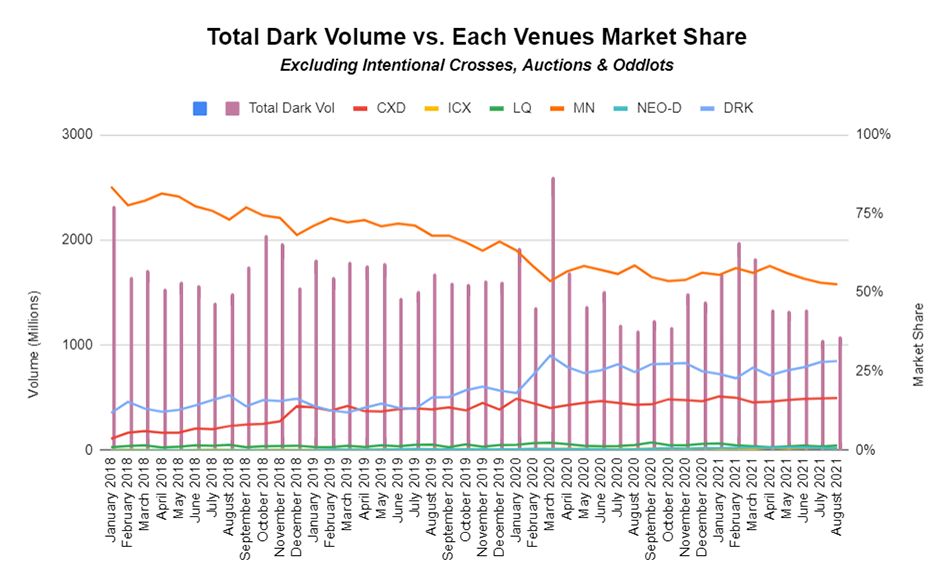

There are currently five dedicated and similar dark markets in Canada, along with TSX DRK™, which have dark order types that can be integrated with our displayed markets.The landscape has become much more competitive, as shown in the chart below, and traders clearly need to access the other pools of dark liquidity in order to achieve best execution for their clients. TSX DRK has made the biggest gains of late in particular with the retail community due to cost savings, deep liquidity and general midpoint price improvement. There is also the additional benefit of the integration of displayed orders taking advantage of price improvement opportunities in TSX DRK without having to intentionally route to a dark market.

Table 2: Market Intelligence Group of TMX Group

How does Canada's dark market compare with other markets?

As compared to other developed equities markets such as the US, EU and Australia, Canada's dark market share is clearly lower for several reasons, particularly regulatory and market structure differences between the regions. It's interesting to note that Australia, which is often compared to Canada, has two exchange-integrated dark pools that account for about 12% of continuous on-market trading and could suggest room for growth in Canada. The EU which went through significant regulatory reform with MiFID II also has considerable dark market share and venues with approximately 16% of pan-European on-venue trading.

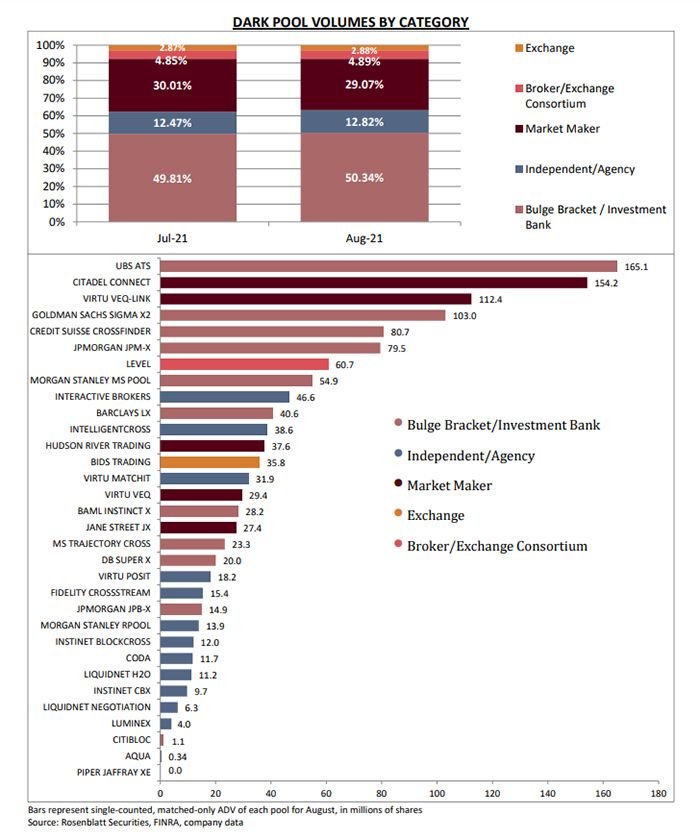

The US dark market is large and dominated by broker-sponsored pools and wholesalers who attempt to internalize flow, which is shown in Table 3 below with nine of ten US dark pools being broker-dealers. This has come under considerable scrutiny of late, as the SEC looks into the practices of wholesaler's payment-for-order-flow (PFOF) and possible manipulation and conflict of interest with best execution. There are 20+ dark venues in the US that represent approximately 14% of equities market share. Given our stricter dark trading rules in Canada, we don't expect to ever get to this number of venues in our market or the inherent market integrity issues associated with broker internalization pools and PFOF.

Table 3: Rosenblatt Securities

What are some of the benefits and strategies for trading in the dark?

There are several factors when considering the benefits of particular markets and strategies to best access available liquidity without displaying intentions. Market participants often consider several factors when configuring their routing tables to the markets. These include, but are not limited to, execution quality, liquidity, trading fees, price improvement, functionality, and venue analysis.

Best execution and quality

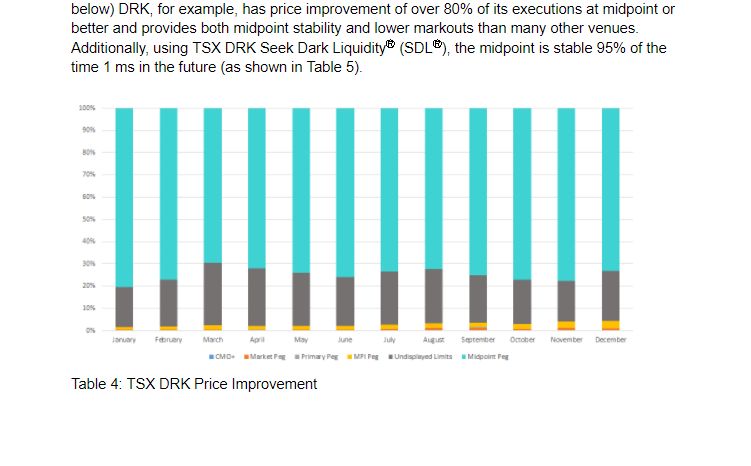

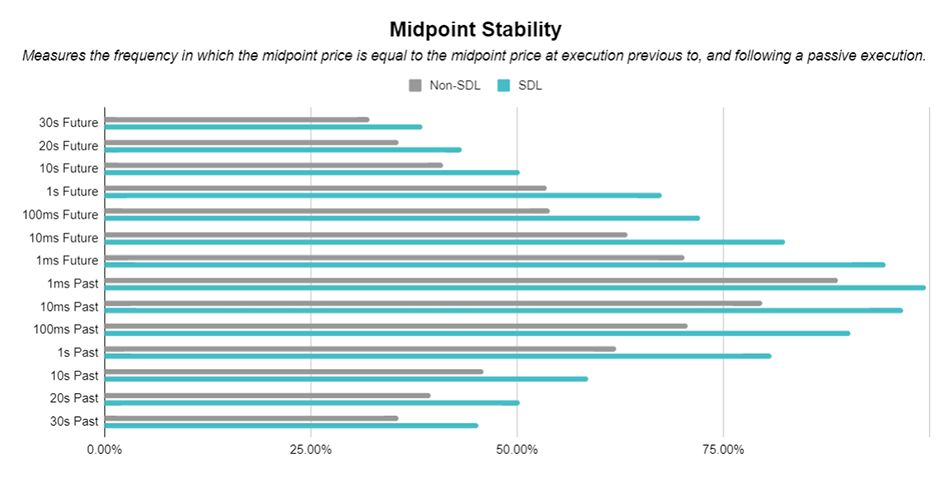

When looking at a dark venue's execution quality, there are a number of metrics that can be used to determine best execution routing strategies. Reversion statistics such as midpoint stability and markouts are often used in analyzing the quality of execution in a dark pool. An important benefit of dark pools is that they generally provide price improvement (i.e., trade within the NBBO or National Best Bid and Offer), and these metrics determine adverse selection and if the trading price has moved away in a period of time since an execution. Midpoint Stability measures how much the price has moved from midpoint after an execution and Markouts measure how much the price has moved from a previous execution. These metrics provide quantifiable data on the quality of execution in the pool. TSX (as shown in Table 4 below) DRK, for example, has price improvement of over 80% of its executions at midpoint or better and provides both midpoint stability and lower markouts than many other venues. Additionally, using TSX DRK Seek Dark LiquidityⓇ (SDLⓇ), the midpoint is stable 95% of the time 1 ms in the future (as shown in Table 5).

Table 4: TSX DRK Price Improvement

Table 5: TSX DRK Midpoint Stability

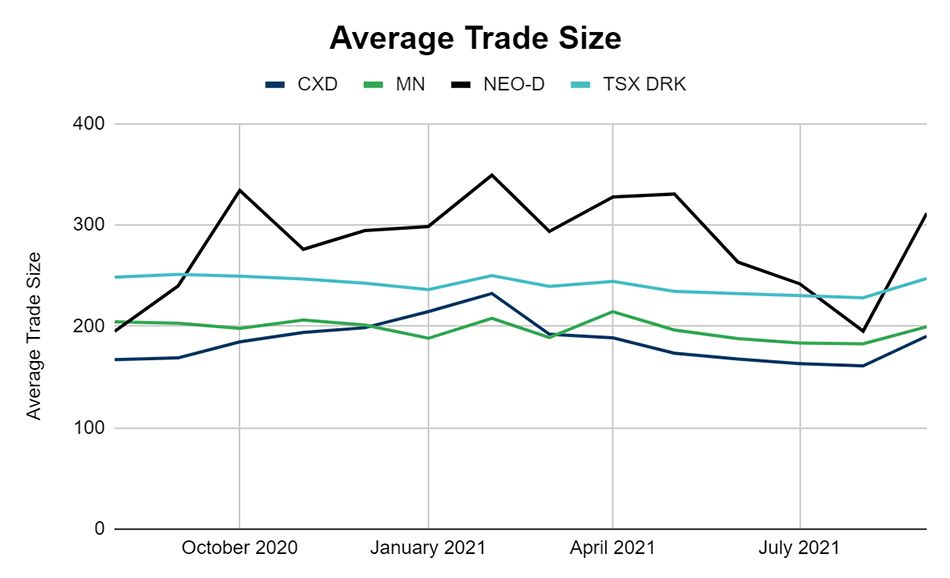

Another consideration when routing to dark markets includes the depth of liquidity in the pool, which determines fill rates and the opportunity to get a good execution in the venue or if integrated with a displayed venue. Average spread and trade size are two other important factors, particularly for institutional traders looking to access larger orders. The average trade size in Canadian dark pools is slightly larger than the displayed venues (as shown in Table 6) and we are starting to see increases with the use of Minimum Quantity and Conditional orders.

Table 6: Average Trade Size in Canadian dark venues (TMX data)

When considering venue analysis, traders may also consider the spreads of the quote and ability to execute within the spread. Spread analysis considers the width of the spread ability to execute within the spread for best execution, but given that these dark markets are not displayed it's difficult to analyze spreads for dark markets. Additionally, and given Canadian markets broker preferencing attributes (i.e. most Canadian markets provide broker preferencing which gives priority to the same broker over the time of entry at the same price), dark venue analysis should consider the ability to internalize order flow. Internalization in the Canadian context can be achieved through broker preferencing and the ability to match active (retail) flow with passive (institutional or market makers), and given the generally favourable dark fee structures can be optimally achieved in many dark pools.

Functionality and trading fees

In today's equities dark markets, as with every business, venues also compete on fees and functionality, and should be considered for inclusion in trading and routing strategies. Trading fees for dark venues are generally less expensive than most displayed marketplaces and can provide cost savings particularly for retail trading and the trend to zero commissions. Most markets have slightly different make/take fees, caps and crossing rates and traders may consider the overall costs of routing when comparing. TSX DRK has the most competitive active dark fees in Canada as compared to other Canadian venues.

Functionality and order types are also an important consideration and benefit to dark pools. Most dark pools offer minimum quantity and pegged order types (primary, market, midpoint, minimum price improvement), which should be considered for larger orders and price improvement. Conditional orders are also becoming more popular in dark pools and provide the opportunity for non-committed large orders; subject to regulatory approval, TSX DRK will be launching Conditional orders in November 2021.

Best practices to access Canadian dark markets

Depth of liquidity is often the most important criteria for marketplace routing tables, but there are other best practices to consider. Because dark markets often provide both cost savings and price improvement, many dealers will route or ping dark pools first, and then route to the various displayed markets. Market routers can be configured to sequentially route to markets or spray multiple markets, but pinging multiple dark pools first is generally considered a good strategy in Canada. In the US, because there are so many dark pools and with varying performance and possible toxicity, traders may be more selective in choosing where to route in the dark.

With the addition of minimum quantity and conditional order types, dark pools should also be considered for larger and block orders. The benefit of using conditional orders in most dark pools, is that institutional traders can limit matches to larger contra conditional orders and signal or leak information of their order. Combined with a minimum size on the order, it can be an effective way of only matching with similar natural block liquidity. Additionally, in conditional pools such as TSX DRK, traders can still integrate with our dark pool and finish up the residual of the order in TSX DRK without the size requirement. This integration of conditional and dark pools is an effective way to manage and complete orders without re-entering or sending more information out to the market. We are just scratching the surface for best practices on dark markets routing strategies and look forward to continuing the discussion in upcoming POVs. Learn more about how Conditionals can improve your dark experience here.

* Unless otherwise noted, all data is sourced from the Market Intelligence Group of TMX Group as of October 21, 2021.

Copyright © 2021 TSX Inc. All rights reserved. Do not copy, distribute, sell or modify this document without TSX Inc.'s prior written consent. This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this publication, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This publication is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. TMX, the TMX design, The Future is Yours to See., Toronto Stock Exchange, TSX, TSX DRK, TSX Venture Exchange, TSXV and Voir le futur. Réaliser l'avenir. are the trademarks of TSX Inc. Seek Dark Liquidity and SDL are the trademarks of Alpha Exchange Inc. and are used under license.